Finance

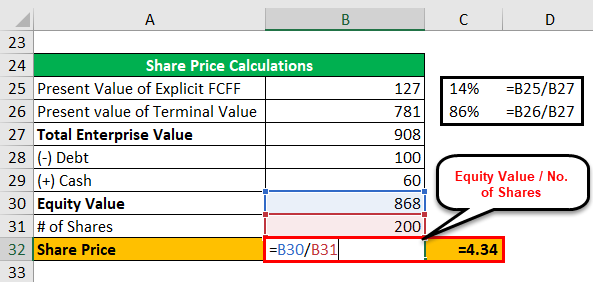

1.Valuation

Corporate Finance, Valuation

2.Factor Calculation for Factor Investment Model

$Common\\,Shareholders'\\,Equity\\,/\\,Market\\,Cap$$Price\\,per\\,Share\\,/EPS=Market\\,Cap\\,/Net\\,Income$$Price\\,per\\,Share\\,/\\,BPS=Market\\,C

3.[Finance] CAPM에 대한 재고

본 포스팅은 기업재무론(Corporate Finance)에서 배우는 CAPM(Capital Asset Pricing Model)을 통계학에서의 선형회귀모델(Linear Statiscal Model)과 연관지어 학습하고자 정리한 시리즈 포스팅입니다 :)CAPM은 간단히

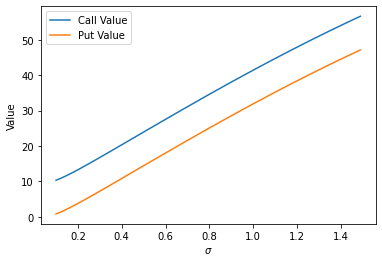

4.Black-Sholes 공식 모델링

$Call$ $=$ $S{0}N(d{1})$ $-$ $N(d2)Ke^{-rT}$ $Put$ $=$ $N(-d{2})Ke^{-rT}$$-$$N(-d{1})S\_{0}$ $d\_{1}$ $=$ $\\frac{ln(S/K)+(r+\\sigma^{2}/2)T}{\\sigma

5.김창기 교수님 금융공학 교재 목차

Source : https://product.kyobobook.co.kr/detail/S000001877202금융공학의 정의금융공학의 범위선도거래(Forward Contracts)선물거래(Futures Contracts)옵션거래스왑거래부도스왑(Default S

6.Lech Grzelak - Computational Finance 강의 및 교재 목차

Source : https://github.com/LechGrzelak/Computational-Finance-Course책 자체는 600페이지 이내로 최병선 교수님, 김창기 교수님 교재보다 많이 얇아서 좋다.Lecture 1- Introduction and

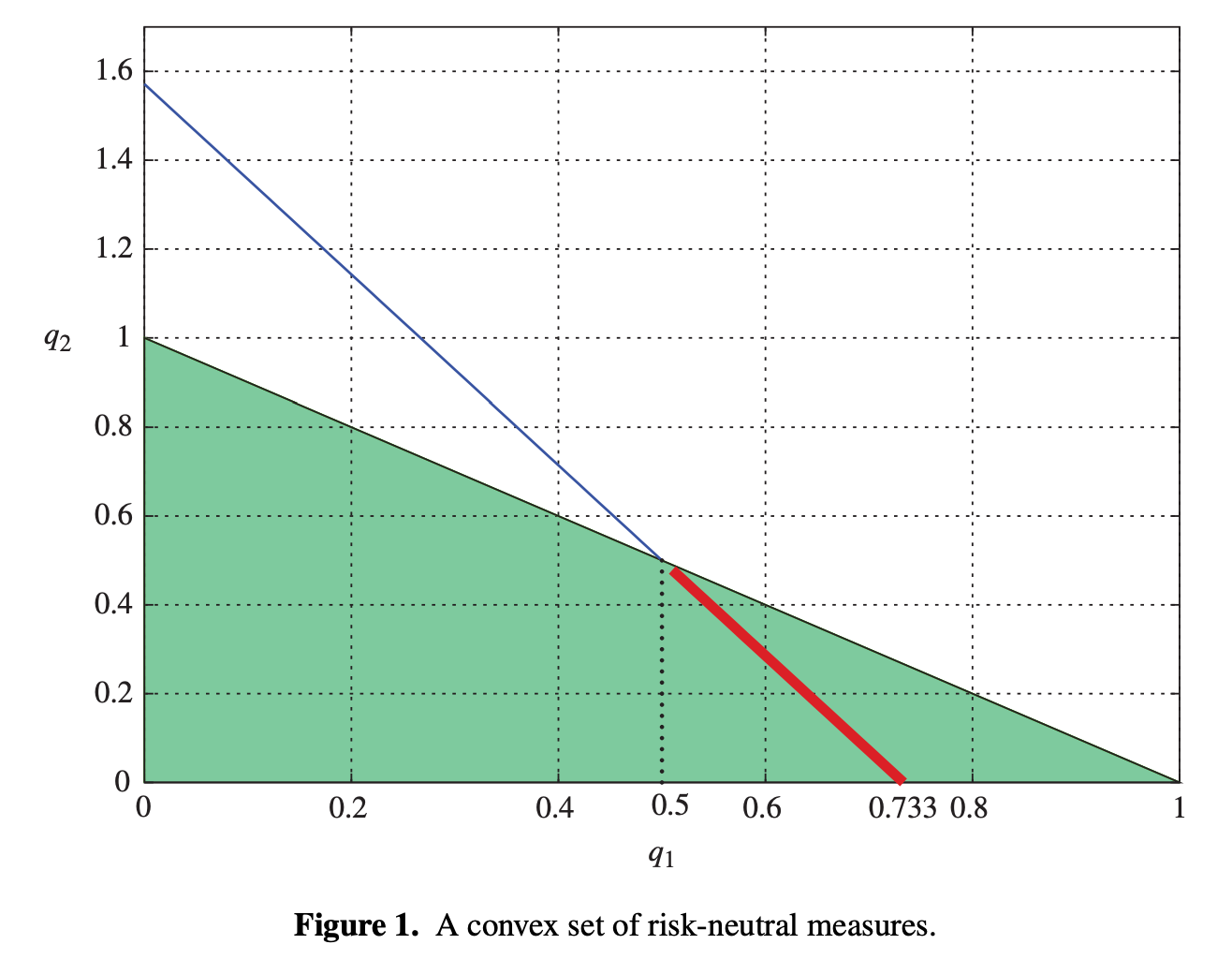

7.Asset Pricing and Linear Algebra

https://doi.org/10.4169/college.math.j.44.1.002Concepts from asset pricing and financial markets theory are used to illustrate concepts of linear

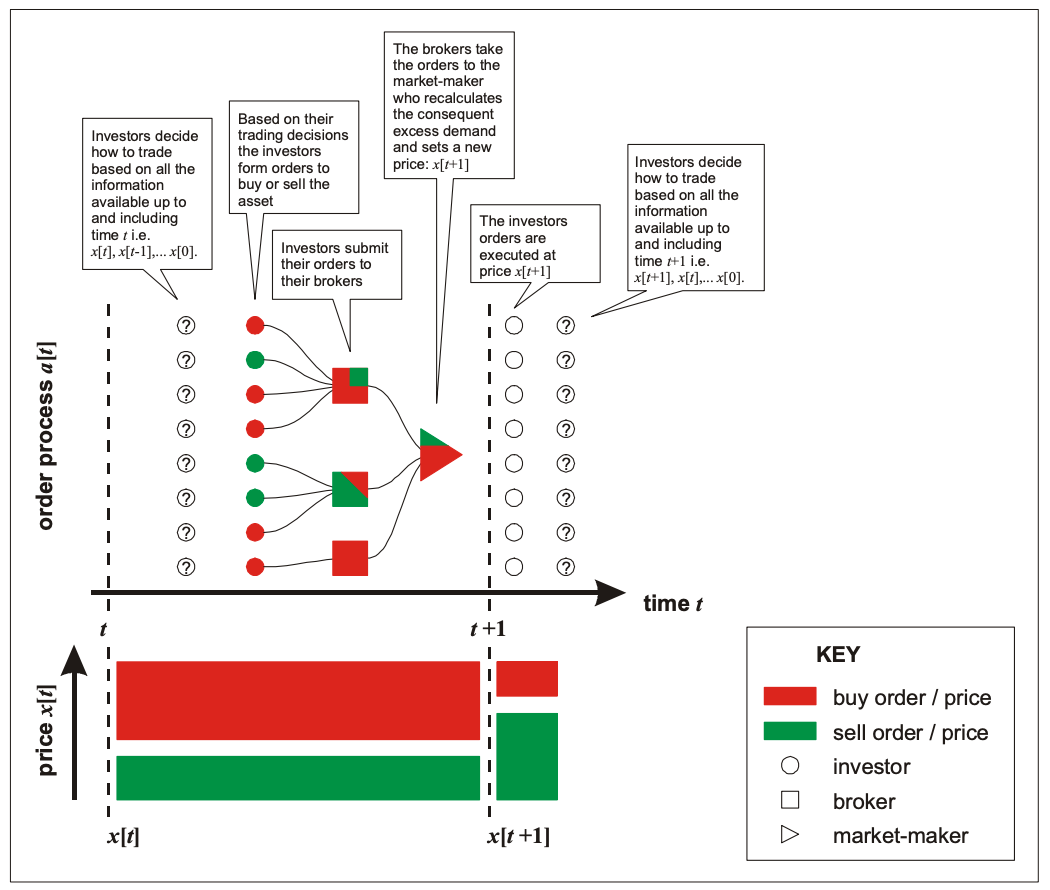

8.Financial Physics (Econophysics) #1 - Financial Markets as complex systems

https://users.physics.ox.ac.uk/~Foot/Phynance/1.1 Real problems in finance1.2 Complex systems and Complexity1.3 Financial market overview1.4 Obse

9.[FICC] Valuation 처돌이의 Quantlib 스터디 (feat. Chat GPT)

주식을 넘어, 이제는 FICC까지 Valuation하는 것에 관심이 많아졌다.Quantlib은 FICC에 대한 Sell-side Pricing 측면에서 가장 강력한 툴로 자리잡고 있기 때문에 Python OOP에 좀만 더 익숙해지고 나면 Quantlib을 열심히 써볼