상점의 아이템 수요예측

데이터

- Store(1,2,3), Item(1,2,3,...), Sales

EDA

- Store 별 Seasonality 체크

- EDA 결과로 적절한 Modeling 선택 가능

Modeling

-

Moving Average

-

Exponential Smoothing

- alpha 조절 잘 해야함 (grid search 관점으로 가도 괜찮을듯)

-

Double Exponential Smoothing

- 식 복잡..ㅋㅋ 나중에 찾아보기

-

Prophet

-

Box-cox

-

ARIMA

FB-prophet

개념

- Time-series forecasting model

- Missing data, shifts in the trend, outlier 에 강함

- 다양한 domain knowledge 에 적용 가능

- trend 가 비선형인 데이터(연도별, 주별, 일별, holiday)에서 자동으로 그 데이터의 변화 포인트를 찍어줌

- 연도별 seasonal component 에는 Fourier series 사용

- 주차별 seasonal component 에는 dummy variables 사용

- important holiday 알려주면 좋음

- g(t) = 부분선형 인 부분 혹은 logistic growth curve(exponential growth) in non-periodic changes in time series

- s(t) = periodic changes( weekly/yearly seasonality)P = 365.25(for yearly data), 7(for weekly data)

a_n, b_n = model seasonality - h(t) = 연휴 혹은 irregular schedule

- εt = unusual change 로 부터 나오는 error

- 즉, non-linear, linear 섞여있을때 regressor 로 fit 해줌

- 시간적 데이터보다 curve 에 더 의존적 인 모델

- Upper bound, lower bound 설정

- 변곡점 잘 세팅해주는게 포인트(business insight 중요)

코드 예시

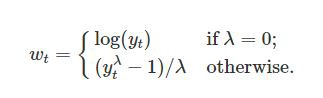

- 상황: digital marketing platform 광고 소비 데이터(fake data 숨겨져있음),

17개월 데이터로 다음 30일 ad spend 예측(2017-06-01~2018-12-30, 577rows, 2columns(date and spend))

from fbprophet import Prophet

sample = pd.read_csv(data위치)

model2=Prophet( interval_width=0.95,

yearly_seasonality=True,

weekly_seasonality=True,

holidays=us_public_holidays,

changepoint_prior_scale=2)

model2.add_seasonality(name=’monthly’, period=30.5, fourier_order=5, prior_scale=0.02)

-> black dots : real data, deep blue line: forecasting numbers, light blue: 95% c.i.

- MAPE or MAE 로 error 측정

Box-Cox Transformation

개념

- Transformations can cut away white noise(Normal distribution으로 만들어줌)

- non-time series data에서도 사용 가능

t = time, lambda = parameter we choose - lambda 는 어떻게 설정할까?

- best normal distribution 을 만들어주는걸로

scipy.special.inv_boxcox(y, lambda)- Box-Cox transformation 의 한계: 해석이 중요한 경우에는 안 좋은 선택

- 결국 y값을 normalization 해주는 느낌 (아래 코드 참고)

train_df2['y'], lambda_prophet = stats.boxcox(train_df2['y'])

train_df2.reset_index(inplace=True)

%%time

m2 = Prophet(yearly_seasonality=True, weekly_seasonality=True, daily_seasonality=True)

m2.fit(train_df2[['ds','y']]);ARIMA

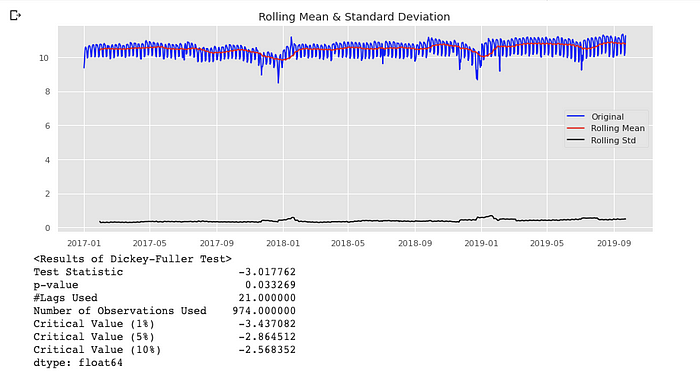

- Non-stationary(constant mean (x), constant variance (x), autocovariance depend on time)

- trend, seasonality 제거하는 방법

- Transformation (log, sqrt...)

- Differencing

- Smoothing (rolling avg...)

- Decomposition

- Polynomial Fitting (fit a regression model)

사진 출처: https://www.slideshare.net/21_venkat?

- AR(Auto Regression) : 이전 데이터를 기반으로 다음 스텝 예측(linear function)

- I (Integration) : stationary 를 만들기 위해

- MA (Moving Average) : 이전 데이터 평균으로 예측

p, d, q 어떻게 결정할까?

- p 를 결정하기 위해 PACF 사용

- q 를 결정하기 위해 ACF 사용

SARIMA (ARIMA + Seasonality)

-

log, diff(1) 을 통해 stationary 하게 만듬

-> log

-> diff

-

code

import statsmodels.api as sm

fit1 = sm.tsa.statespace.SARIMAX(train.Spend, order=(7, 1, 2), seasonal_order=(0, 1, 2, 7)).fit(use_boxcox=True)

test['SARIMA'] = fit1.predict(start="2019-07-23", end="2019-09-23", dynamic=True)

plt.figure(figsize=(16, 8))

plt.plot(train['Spend'], label='Train')

plt.plot(test['Spend'], label='Test')

plt.plot(test['SARIMA'], label='SARIMA')

plt.legend(loc='best')

plt.show()Holt-Winter's Seasonal Smoothing(one of exponential smoothing)

from statsmodels.tsa.api import ExponentialSmoothing

fit1 = ExponentialSmoothing(np.asarray(train['Spend']) ,seasonal_periods=7 ,trend='add', seasonal='add').fit(use_boxcox=True)

test['Holt_Winter'] = fit1.forecast(len(test))

plt.figure(figsize=(16,8))

plt.plot( train['Spend'], label='Train')

plt.plot(test['Spend'], label='Test')

plt.plot(test['Holt_Winter'], label='Holt_Winter')

plt.legend(loc='best')

plt.show()

Data Scientist or Gourmet