- Pandas was originally developed in the context of financial modeling, so it contains an extensive set of tools for working dates, times, and time-indexed data.

- Timestamps : Particular moments in time

- Time interval and periods : A length of time between a particular beginning and end point

- Time deltas or durations : An exact length of time

Dates and Times in Python

Native Python Dates and Times: datetime and dateutil

# In[1]

from datetime import datetime

datetime(year=2023,month=7,day=28)# Out[1]

datetime.datetime(2023, 7, 28, 0, 0)- Or, using the

dateutilmodule, you can parse dates from a variety of string formats.

# In[2]

from dateutil import parser

date=parser.parse("28th of July, 2023")

date# Out[2]

datetime.datetime(2023, 7, 28, 0, 0)- Using

datetimeobject, you can do things like printing the day of the week.

# In[3]

date.strftime('%A')# Out[3]

'Friday'Typed Arrays of Times: Numpy's datetime64

- Numpy's

datetime64dtype encodes dates as 64-bit integers, and thus allows arrays of dates to be represented compactly and operated on in an efficient manner. - It requires a specific input format

# In[4]

date=np.array('2023-07-28',dtype=np.datetime64)

date# Out[4]

array('2023-07-28', dtype='datetime64[D]')- We can quickly do vectorized operations on it.

# In[5]

date+np.arange(12)# Out[5]

array(['2023-07-28', '2023-07-29', '2023-07-30', '2023-07-31',

'2023-08-01', '2023-08-02', '2023-08-03', '2023-08-04',

'2023-08-05', '2023-08-06', '2023-08-07', '2023-08-08'],

dtype='datetime64[D]')- This kind of operation can be accomplished much more quickly than if we were working directly with Python's

datetimeobjects, especially as arrays get large.

- One detail of the

datetime64and relatedtimedelta64objects is that they are built on a fundamental time unit. - The

datetime64object is limited to 64-bit precision, the range of encodable times is times this fundamental unit. datetime64imposes a trade-off between time resolution and maximum time span.

# In[6]

print(np.datetime64('2023-07-28')) # day based

print(np.datetime64('2023-07-28 12:00')) # minute based

print(np.datetime64('2023-07-28 12:59:59.50','ns')) # nanosecond based# Out[6]

2023-07-28

2023-07-28T12:00

2023-07-28T12:59:59.500000000- More informations about

datetime64can be found in Numpy's datatime64 documentation

Dates and Times in Pandas: The Best of Both Worlds

- Pandas builds upon all the tools just discussed to provide a

Timestampobject, which combines the ease of use ofdatetimeanddateutilwith the efficient storage and vectorized interface ofnumpy.datetime64 - From a group of these

Timestampobjects, Pandas can construct a DatetimeIndex that can be used to index data in a Series or DataFrame.

# In[7]

date=pd.to_datetime("28th of July, 2023")

date# Out[7]

Timestamp('2023-07-28 00:00:00')# In[8]

date.strftime('%A')# Out[8]

'Friday'- We can do Numpy-style vectorized operations directly on this same object.

# In[9]

date+pd.to_timedelta(np.arange(12),'D')# Out[9]

DatetimeIndex(['2023-07-28', '2023-07-29', '2023-07-30', '2023-07-31',

'2023-08-01', '2023-08-02', '2023-08-03', '2023-08-04',

'2023-08-05', '2023-08-06', '2023-08-07', '2023-08-08'],

dtype='datetime64[ns]', freq=None)Pandas Time Series: Indexing by Time

- The Pandas time series tools really become useful when you begin to index date by timestamps.

# In[10]

index=pd.DatetimeIndex(['2023-07-28','2023-08-28',

'2024-07-28','2024-08-28'])

data=pd.Series([0,1,2,3],index=index)

data# Out[10]

2023-07-28 0

2023-08-28 1

2024-07-28 2

2024-08-28 3

dtype: int64- We can make use of any of the Series indexing patterns, passing values that can be coerced(=force) into dates.

# In[11]

data['2023-07-28':'2024-07-28']# Out[11]

2023-07-28 0

2023-08-28 1

2024-07-28 2

dtype: int64- There are additional special date-only indexing operations, such as passing a year to obtain a slice of all data from that year.

# In[12]

data['2023']# Out[12]

2023-07-28 0

2023-08-28 1

dtype: int64Pandas Time Series: Data Structure

-

For timestamps, Pandas provides the

Timestamptype.- This is essentially a replacement for Python's native

datetime, but it's based on the more effcientnp.datetime64data type. - Associated Index structure is

DatetimeIndex

- This is essentially a replacement for Python's native

-

For time periods, Pandas provides the

Periodtype.- This encodes a fixed-frequency interval based on

np.datetime64 - Associated index structure is

PeriodIndex

- This encodes a fixed-frequency interval based on

-

For time deltas or durations, Pandas provides the

Timedeltatype.- It is a more efficient replacement for Python's native

datetime.timedeltatype, and is based onnp.timedelta64 - Associated index structure is

TimedeltaIndex

- It is a more efficient replacement for Python's native

-

Commonly, we use the

pd.to_datetimefunction, which can parse(=analyze) a wide variety of formats. -

Passing a single date to

pd.to_datetimeyields a Timestamp.

# In[13]

dates=pd.to_datetime([datetime(2023,7,28),'28th of July, 2023',

'2023-07-30','31-07-2023','20230801'])

dates# Out[13]

DatetimeIndex(['2023-07-28', '2023-07-28', '2023-07-30', '2023-07-31',

'2023-08-01'],

dtype='datetime64[ns]', freq=None)- Any DatetimeIndex can be converted to a PeriodIndex with the

to_periodfunction, with the addition of a frequency code.

# In[14]

dates.to_period('D')# Out[14]

PeriodIndex(['2023-07-28', '2023-07-28', '2023-07-30', '2023-07-31',

'2023-08-01'],

dtype='period[D]')- A TimedeltaIndex is created when a date is subtracted from another.

# In[15]

dates-dates[0]# Out[15]

TimedeltaIndex(['0 days', '0 days', '2 days', '3 days', '4 days'], dtype='timedelta64[ns]', freq=None)Regular Sequences: pd.date_range

- To make creation of regular date sequences more convenient, Pandas offers a few functions for this purpose

pd.date_rangefor timestampspd.period_rangefor periodspd.timedelta_rangefor time deltas.

# In[16]

pd.date_range('2023-07-28','2023-08-14')# Out[16]

DatetimeIndex(['2023-07-28', '2023-07-29', '2023-07-30', '2023-07-31',

'2023-08-01', '2023-08-02', '2023-08-03', '2023-08-04',

'2023-08-05', '2023-08-06', '2023-08-07', '2023-08-08',

'2023-08-09', '2023-08-10', '2023-08-11', '2023-08-12',

'2023-08-13', '2023-08-14'],

dtype='datetime64[ns]', freq='D')- The date range can be specified not with a start and end point, but with a start point and a number of periods.

# In[17]

pd.date_range('2023-07-28',periods=8)# Out[17]

DatetimeIndex(['2023-07-28', '2023-07-29', '2023-07-30', '2023-07-31',

'2023-08-01', '2023-08-02', '2023-08-03', '2023-08-04'],

dtype='datetime64[ns]', freq='D')- The spacing can be modified by altering the

freqargument, which defaults toD.

# In[18]

pd.date_range('2023-07-28',periods=8,freq='H')# Out[18]

DatetimeIndex(['2023-07-28 00:00:00', '2023-07-28 01:00:00',

'2023-07-28 02:00:00', '2023-07-28 03:00:00',

'2023-07-28 04:00:00', '2023-07-28 05:00:00',

'2023-07-28 06:00:00', '2023-07-28 07:00:00'],

dtype='datetime64[ns]', freq='H')- To create regular sequence of Period or Timedelta values, the similar

pd.period_rangeandpd.timedelta_rangefunctions are useful.

# In[19]

pd.period_range('2023-07',periods=8,freq='M')# Out[19]

PeriodIndex(['2023-07', '2023-08', '2023-09', '2023-10', '2023-11', '2023-12',

'2024-01', '2024-02'],

dtype='period[M]')# In[20]

pd.timedelta_range(0,periods=6,freq='H')# Out[20]

TimedeltaIndex(['0 days 00:00:00', '0 days 01:00:00', '0 days 02:00:00',

'0 days 03:00:00', '0 days 04:00:00', '0 days 05:00:00'],

dtype='timedelta64[ns]', freq='H')Frequencies and Offsets

- Fundamental to these Pandas time series tools is the concept of a frequency or date offset.

Listing of Pandas frequency codes

| Code | Description | Codes | Description |

|---|---|---|---|

D | Calendar day | B | Business day |

W | Weekly | ||

M | Month end | BM | Business month end |

Q | Quarter end | BQ | Business quarter end |

A | Year end | BA | Business year end |

H | Hours | BH | Business hours |

T | Minutes | ||

S | Seconds | ||

L | Milliseconds | ||

U | Microseconds | ||

N | Nanoseconds |

- The monthly, quarterly, and annual frequencies are all marked at the end of the specified period.

Listing of start-indexed frequency codes

| Code | Description |

|---|---|

MS | Month start |

QS | Quarter start |

AS | Year start |

BS | Business month start |

BQS | Business quarter start |

BAS | Business year start |

-

Additionally, you can change the month used to mark any quarterly or annual code by adding a three-letter month code as a suffix.

Q-JAN,BQ-FEB,QS-MAR,BQS-APRetc.

-

In the same way, the split point of the weekly frequency can be modified by adding a three-letter weekday code.

W-SUN,W-MON,W-TUE,W-WEDetc.

-

Codes can be combined with numbers to specify otehr frequencies.

# In[21]

pd.timedelta_range(0,periods=6,freq='2H30T')# Out[21]

TimedeltaIndex(['0 days 00:00:00', '0 days 02:30:00', '0 days 05:00:00',

'0 days 07:30:00', '0 days 10:00:00', '0 days 12:30:00'],

dtype='timedelta64[ns]', freq='150T')- All of these short codes refer to specific instances of Pandas time series offsets, which can be found in the

pd.tseries.offsetsmodule.

# In[22]

from pandas.tseries.offsets import BDay

pd.date_range('2023-07-28',periods=6,freq=BDay())# Out[22]

DatetimeIndex(['2023-07-28', '2023-07-31', '2023-08-01', '2023-08-02',

'2023-08-03', '2023-08-04'],

dtype='datetime64[ns]', freq='B')- For more information about the use of frequencies and offsets, see the DateOffset section of the Pandas documentation

Resampling, Shifting, and Windowing

- The ability to use dates and times as indices to intuitively organize and access data is an important aspect of the Pandas time series tools.

- The benefits of indexed data in general still apply, and Pandas provides several additional time series-specific operations.

# In[23]

import pandas_datareader.data as web

start_date = datetime(2006, 1, 1)

end_date = datetime(2016, 1, 1)

#Bank of America

bac = data.DataReader('BAC', 'stooq', start_date, end_date)

bac.head()# Out[23]

Open High Low Close Volume

Date

2015-12-31 14.7814 14.8325 14.6233 14.6233 5.417059e+07

2015-12-30 14.9473 14.9807 14.8070 14.8168 4.030734e+07

2015-12-29 14.9897 15.0780 14.9130 15.0131 5.251059e+07

2015-12-28 14.9630 14.9720 14.7539 14.8846 4.803435e+07

2015-12-24 15.0495 15.1035 14.9630 15.0063 3.380344e+07# In[24]

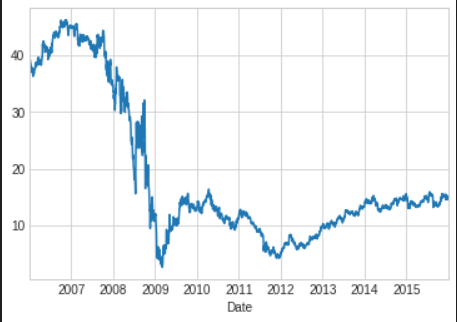

bac=bac['Close']- We can visualize this using the

plotmethod.

# In[25]

%matplotlib inline

import matplotlib.pyplot as plt

plt.style.use('seaborn-whitegrid')

bac.plot();

Resampling and Converting Frequencies

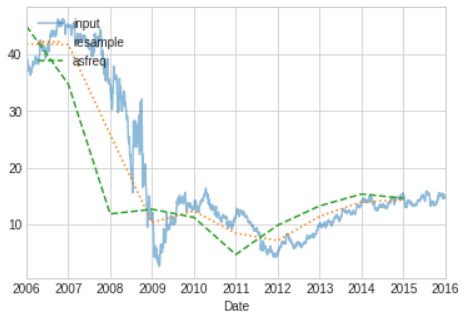

- One common need when dealing with time series data is resampling at a higher or lower frequency.

- This can be done using the

resamplemethod, or the much simplerasfreqmethod. - The primary difference between the two is that

resampleis fundamentally a data aggregation, whileasfreqis fundamentally a data selection.

# In[26]

bac.plot(alpha=0.5,style='-')

bac.resample('BA').mean().plot(style=':')

bac.asfreq('BA').plot(style='--')

plt.legend(['input','resample','asfreq'],loc='upper left');

resamplereports the average of the previous year, whileasfreqreports the value at the end of the year.

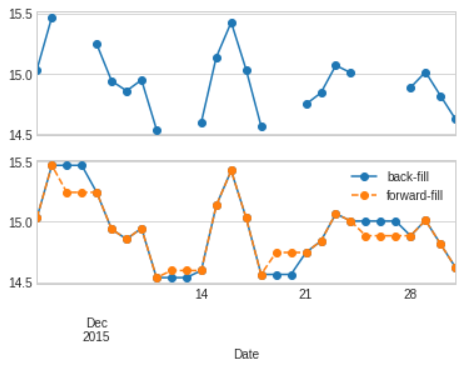

- For upsampling,

resampleandasfreqare largely equivalent, thoughresamplehas many more options available. - Like the

pd.fillnafunction,asfreqaccepts a method argument to specify how values are imputed.

# In[27]

fig, ax=plt.subplots(2,sharex=True)

data=bac.iloc[:20]

data.asfreq('D').plot(ax=ax[0],marker='o')

data.asfreq('D',method='bfill').plot(ax=ax[1],style='-o')

data.asfreq('D',method='ffill').plot(ax=ax[1],style='--o')

ax[1].legend(["back-fill","forward-fill"]);

- The bottom panel shows the differences between two strategies for filling the gaps: forward filling and backward filling

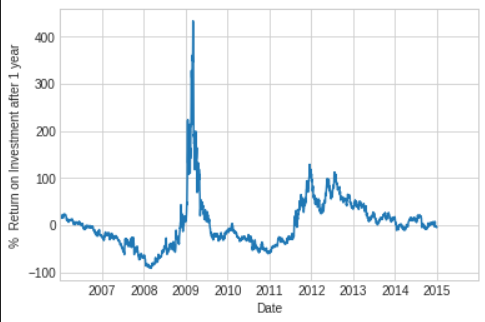

Time Shifts

- Another common tine series-specific operation is shifting of data in time.

- For this, Pandas provides the

shiftmethod, which can be used to shift data by a given number of entries.

# In[28]

bac=bac.asfreq('D',method='pad')

ROI=100*(bac.shift(-365)-bac)/bac

ROI.plot()

plt.ylabel('% Return on Investment after 1 year');

Rolling Windows

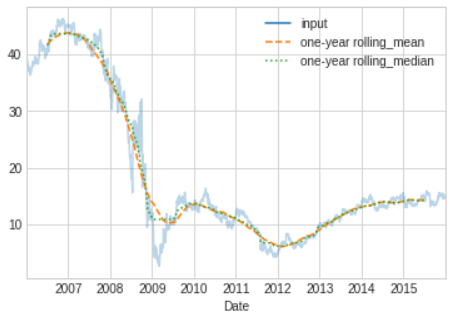

- Calculating rolling statistics is a third type of time series-specific operation implemented by Pandas.

- This can be accomplished via the

rollingattribute of Series and DataFrame object, which returns a view similar to what we saw with the groupby operation. - This rolling view makes available a number of aggregation operations by default.

# In[29]

rolling=bac.rolling(365,center=True)

data=pd.DataFrame({'input':bac,'one-year rolling_mean':rolling.mean(),

'one-year rolling_median':rolling.median()})

ax=data.plot(style=['-','--',':'])

ax.lines[0].set_alpha(0.3)

- As with groupby operations, the aggregate and apply methods can be used for custom rolling computations.

- For a more complete discussion, you can refer to the

Time Series/Date Functionality section of the Pandas online documentation

노정훈