permutaion importances

- 특정 노이즈 전후 성능 비교

boosting

- 베깅: 트리 독립적인가 아닌가?

- ada boost,gb -> xgb

XAI

모델 A -> 설명x

모델 B -> 설명O

설명 되는 모델 B를 픽할 것임

pdp

- 특성 a : 결과에 어떻게 영향?

shap

- 특성 a,b,c,d: 개별 샘플에 어떻게 영향?>summary plot

PDP(Partial dependence plots)

- 랜덤/부스팅/딥러닝 모델은 내부에서 정해지는 결정과정은 이해하기 어렵기 때문에 블랙박스 모델이라고도함

- 트리 모델 학습-특성 중요도로 특성확인할 수 있지만 트리에만 국한되는것임

- 퍼뮤테이션 임포턴스 : 학습 모델 종류와 상관없이 모델을 설명할 때 사용할 수 있는 모델 애그노스틱 방법임

복잡한 모델>이해하기 어렵지만 성능이 좋음

단순한 모델>이해가 쉬운데 성능이 부족

pdp는 특성값에 따라서 타겟값이 증가/감소하는 정보를 알 수가 있음

- 특성들을 선형적으로 변환 시켜보면서 타겟이 어떻게 변화(증감)하느지 시각화 하여 보는 방법

%%capture

# Ignore this warning: https://github.com/dmlc/xgboost/issues/4300

# xgboost/core.py:587: FutureWarning: Series.base is deprecated and will be removed in a future version

import warnings

warnings.filterwarnings(action='ignore', category=FutureWarning, module='xgboost')

import pandas as pd

# Kaggle 데이터세트에서 10% 샘플링된 데이터입니다.

## Source: https://www.kaggle.com/wordsforthewise/lending-club

## 10% of expired loans (loan_status: ['Fully Paid' and 'Charged Off'])

## grades A-D

## term ' 36 months'

df = pd.read_csv('https://ds-lecture-data.s3.ap-northeast-2.amazonaws.com/lending_club/lending_club_sampled.csv')

df['issue_d'] = pd.to_datetime(df['issue_d'], infer_datetime_format=True)

# issue_d로 정렬

df = df.set_index('issue_d').sort_index()

df['interest_rate'] = df['int_rate'].astype(float)

df['monthly_debts'] = df['annual_inc'] / 12 * df['dti'] / 100

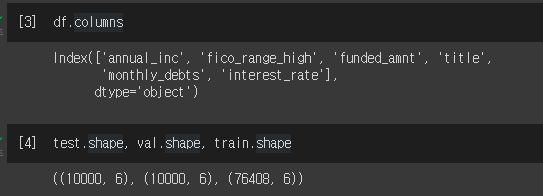

# 152 특성 중 6특성만 사용

columns = ['annual_inc', # 연수입

'fico_range_high', # 신용점수

'funded_amnt', # 대출

'title', # 대출 목적

'monthly_debts', # 월간 부채

'interest_rate'] # 이자율

df = df[columns]

df = df.dropna()

# 마지막 10,000 대출은 테스트셋

# 테스트셋 전 10,000 대출이 검증셋

# 나머지는 학습셋

test = df[-10000:]

val = df[-20000:-10000]

train = df[:-20000]df.columns, test.shape, val.shape, train.shape

선형회귀로 알아보기

!pip install --upgrade category_encoders

from category_encoders import TargetEncoder

from sklearn.linear_model import LinearRegression

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import StandardScaler

linear = make_pipeline(

TargetEncoder(),

LinearRegression()

)

linear.fit(X_train, y_train)

print('R^2', linear.score(X_val, y_val))

#R^2 0.1758506495816231 값이 작음

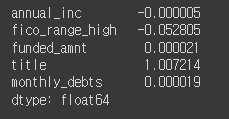

# 회귀계수 확인

coefficients = linear.named_steps['linearregression'].coef_

pd.Series(coefficients, features)

그래디언트 부스팅으로 학습진행

from category_encoders import OrdinalEncoder

from sklearn.metrics import r2_score

from xgboost import XGBRegressor

encoder = OrdinalEncoder()

X_train_encoded = encoder.fit_transform(X_train) # 학습데이터

X_val_encoded = encoder.transform(X_val) # 검증데이터

boosting = XGBRegressor(

n_estimators=1000,

objective='reg:squarederror', # default

learning_rate=0.2,

n_jobs=-1

)

eval_set = [(X_train_encoded, y_train),

(X_val_encoded, y_val)]

boosting.fit(X_train_encoded, y_train,

eval_set=eval_set,

early_stopping_rounds=50

)

y_pred = boosting.predict(X_val_encoded)

print('R^2', r2_score(y_val, y_pred))

#R^2 0.228134736099475 선형보다 성능 좋아짐그래디언트 부스팅 결과를 해석하려면?

선형모델은 회귀계수를 이용해 변수와 타겟 관계를 해석할 수 있지만 트리모델은 할 수 없음

- 대신 부분의존그림을 사용하여 개별 특성과 타겟간의 관게를 볼 수 있음

PDP (1개의 특성 사용)

pip install PDPbox

# dpi(dots per inch) 수치를 조정해 이미지 화질을 조정 할 수 있습니다

import matplotlib.pyplot as plt

plt.rcParams['figure.dpi'] = 144

from pdpbox.pdp import pdp_isolate, pdp_plot

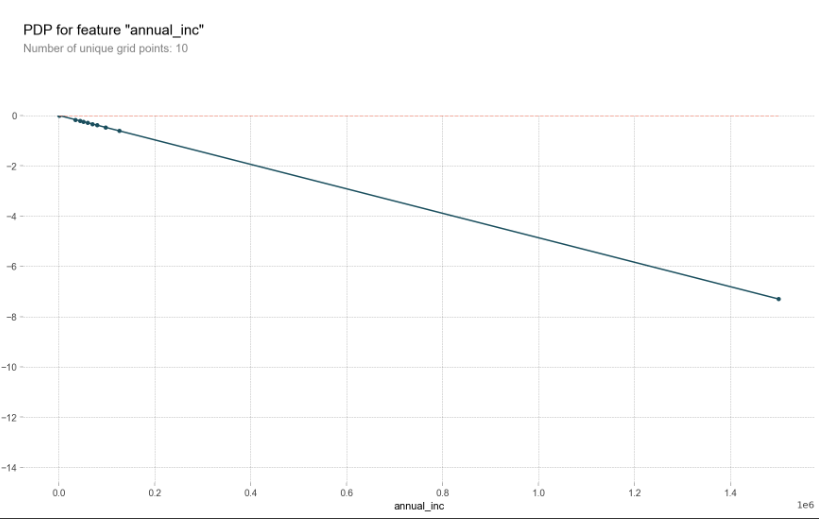

feature = 'annual_inc'

isolated = pdp_isolate(

model=linear,

dataset=X_val,

model_features=X_val.columns,

feature=feature,

grid_type='percentile', # default='percentile', or 'equal'

num_grid_points=10 # default=10

)

pdp_plot(isolated, feature_name=feature);

그래디언트 부스팅 모델에서 annual_inc PDP를 그려봄

isolated = pdp_isolate(

model=boosting,

dataset=X_val_encoded,

model_features=X_val_encoded.columns,

feature=feature

)

pdp_plot(isolated, feature_name=feature);

변화량부분에서 이자율이 급격하게 떨어진다.

pdp_plot(isolated, feature_name=feature)

plt.xlim((20000,150000));

pdp를 10개의 ice(individual conditional expectation)curves와 함께 그려봄

한 ice곡선은 하나의 관측치에 대해 관심 특성을 변화시킴에 따른 타겟값 변화 곡선이고 이 ice들의 평균이 pdp입니다.

pdp_plot(isolated

, feature_name=feature

, plot_lines=True # ICE plots

, frac_to_plot=0.001 # or 10 (# 10000 val set * 0.001)

, plot_pts_dist=True)

plt.xlim(20000,150000);

Ice curves->PDP를 표현하는 GIF

한특성에 대해 pdp를 그릴 경우 얼마나 많은 예측이 필요할까요?

데이터셋 사이즈에 grid points를 곱한 수 만큼 예측을 해야함

isolated = pdp_isolate(

model=boosting,

dataset=X_val_encoded,

model_features=X_val.columns,

feature=feature,

# grid point를 크게 주면 겹치는 점이 생겨 Number of unique grid points는 grid point 보다 작을 수 있습니다.

num_grid_points=100, # grid 포인트를 더 줄 수 있습니다. default = 10

)

print('예측수: ',len(X_val) * 100)

#예측수: 1000000

pdp_plot(isolated

, feature_name=feature

, plot_lines=True

, frac_to_plot=0.01 # ICE curves는 100개

, plot_pts_dist=True )

plt.xlim(20000,150000);

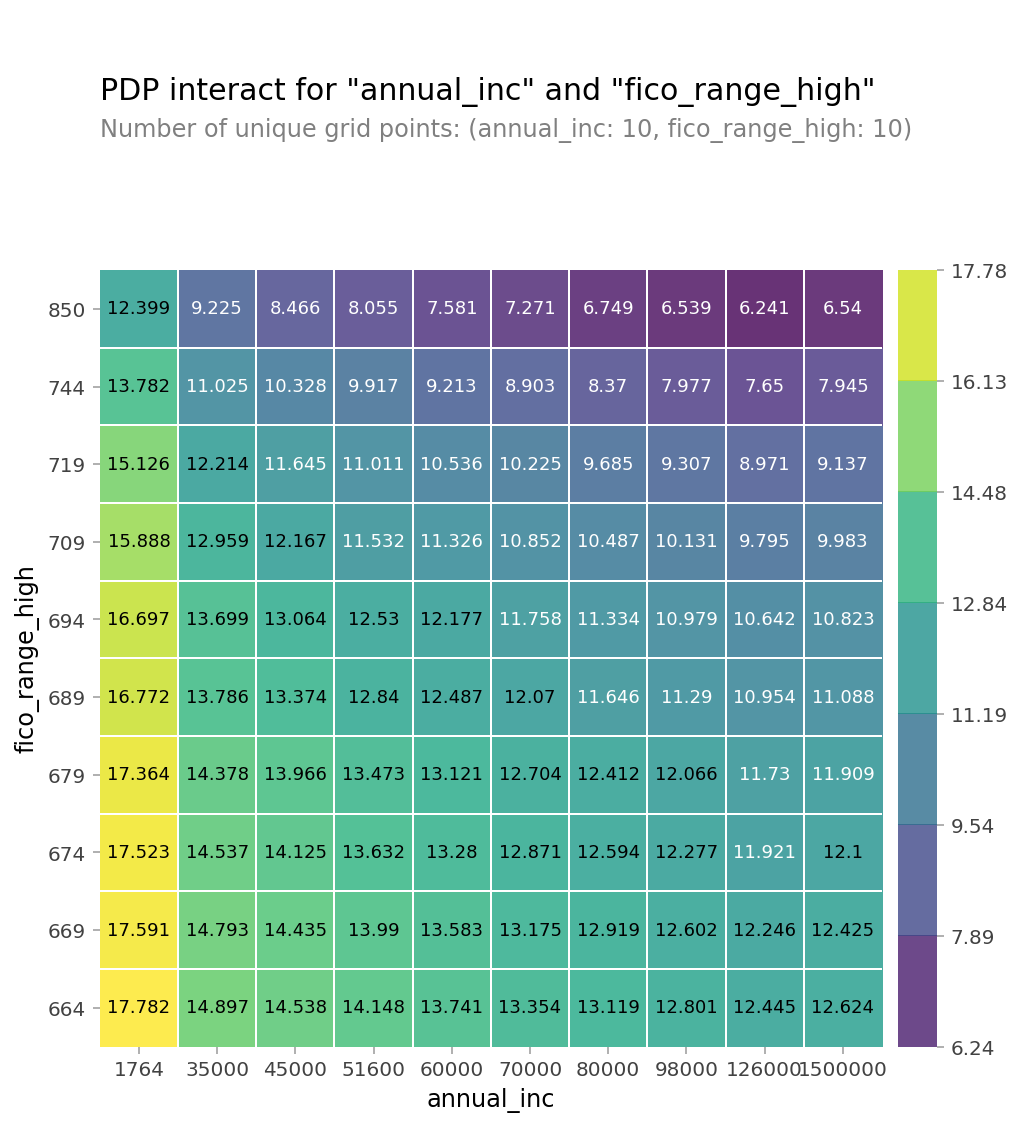

PDP (2개의 특성 사용)

- 두 특성간의 상호작용을 pdp를 통해 확인

from pdpbox.pdp import pdp_interact, pdp_interact_plot

features = ['annual_inc', 'fico_range_high']

interaction = pdp_interact(

model=boosting,

dataset=X_val_encoded,

model_features=X_val.columns,

features=features

)

pdp_interact_plot(interaction, plot_type='grid',

feature_names=features);

PDP에서 카테고리특성을 사용

카테고리 특성을 학습할 대 Ordinal Encoder, Target Encoder 같은 인코더를 사용하게됨

인코딩을 하게되면 학습 후 PDP를 그릴 때 인코딩된 값이 나오게 되어 카테고리특성의 실제 값을 확인하기 어려운 문제가 있습니다.

이번에는 pdp에 인코딩되기 전 카테고리값을 보여주기 위한 방법을 아아보겠습니다.

import seaborn as sns

from sklearn.ensemble import RandomForestClassifier

from sklearn.pipeline import make_pipeline

df = sns.load_dataset('titanic')

df['age'] = df['age'].fillna(df['age'].median())

df = df.drop(columns='deck') # NaN 77%

df = df.dropna()

target = 'survived'

features = df.columns.drop(['survived', 'alive'])

X = df[features]

y = df[target]

pipe = make_pipeline(

OrdinalEncoder(),

RandomForestClassifier(n_estimators=100, random_state=42, n_jobs=-1)

)

pipe.fit(X, y);

encoder = pipe.named_steps['ordinalencoder']

X_encoded = encoder.fit_transform(X)

rf = pipe.named_steps['randomforestclassifier']

import matplotlib.pyplot as plt

from pdpbox import pdp

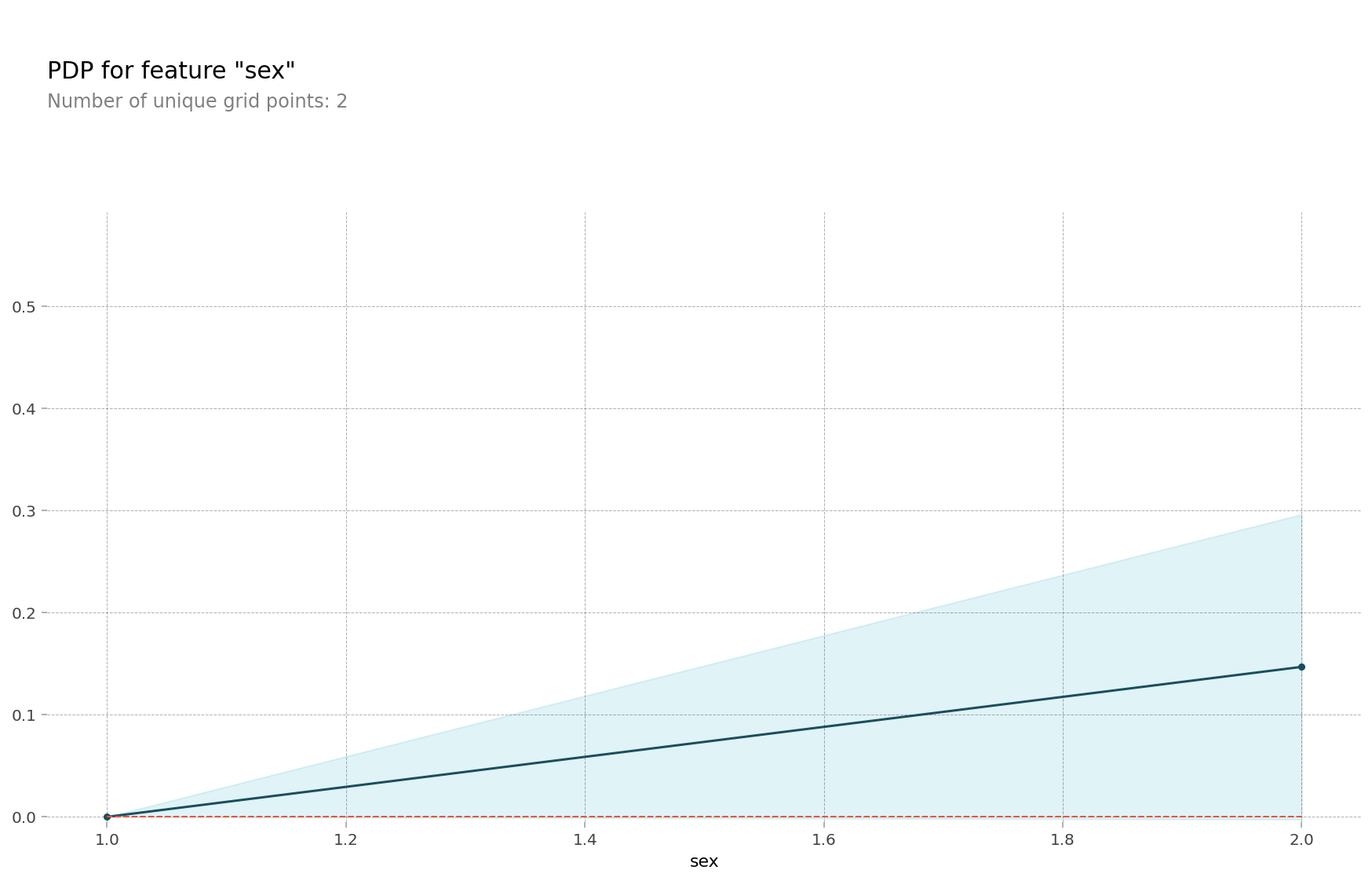

feature = 'sex'

pdp_dist = pdp.pdp_isolate(model=rf, dataset=X_encoded, model_features=features, feature=feature)

pdp.pdp_plot(pdp_dist, feature); # 인코딩된 sex 값을 확인할 수 있습니다

# encoder 맵핑을 확인합니다, {male:1, female:2} 로 인코딩 되어 있습니다

encoder.mapping

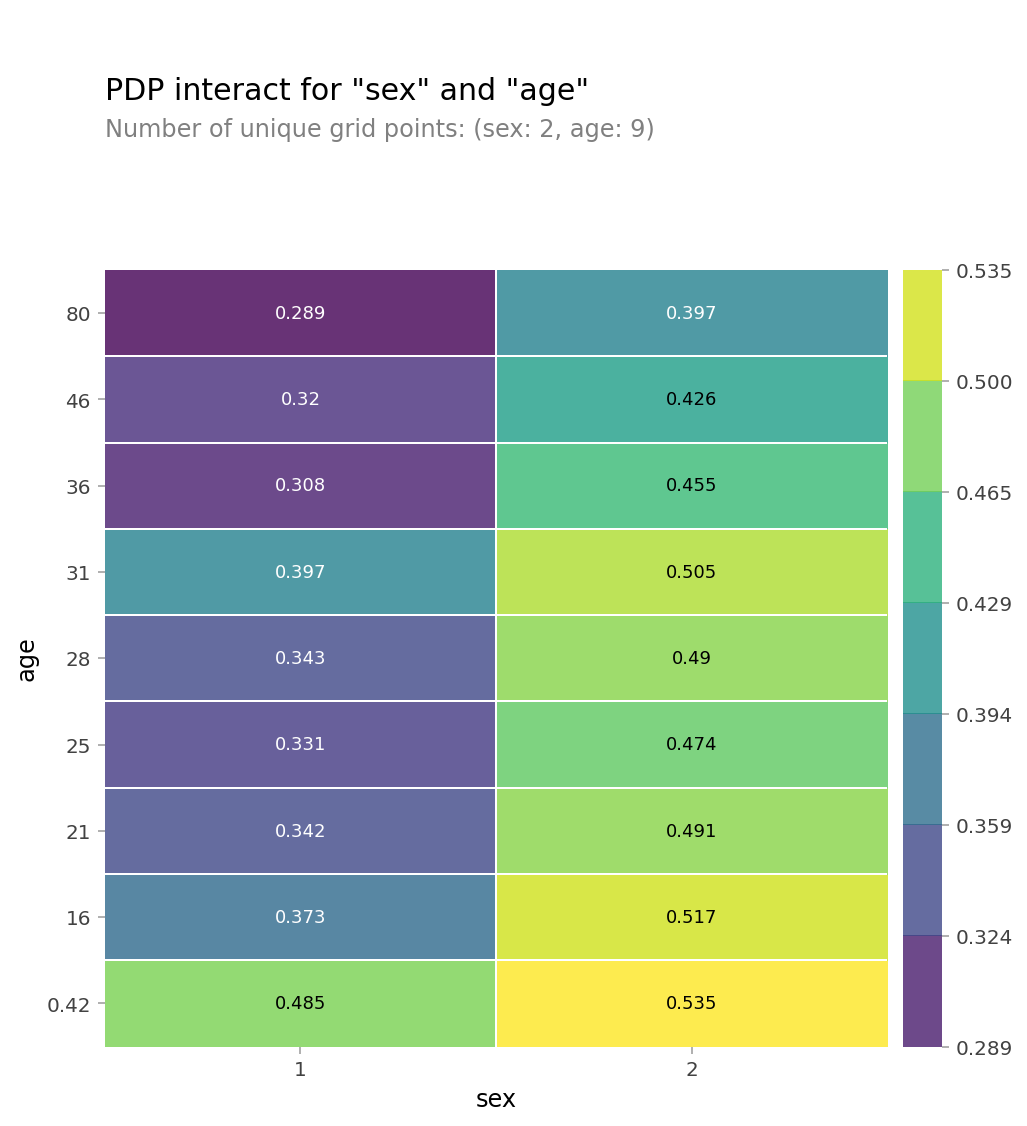

# 2D PDP

features = ['sex', 'age']

interaction = pdp_interact(

model=rf,

dataset=X_encoded,

model_features=X_encoded.columns,

features=features

)

pdp_interact_plot(interaction, plot_type='grid', feature_names=features);

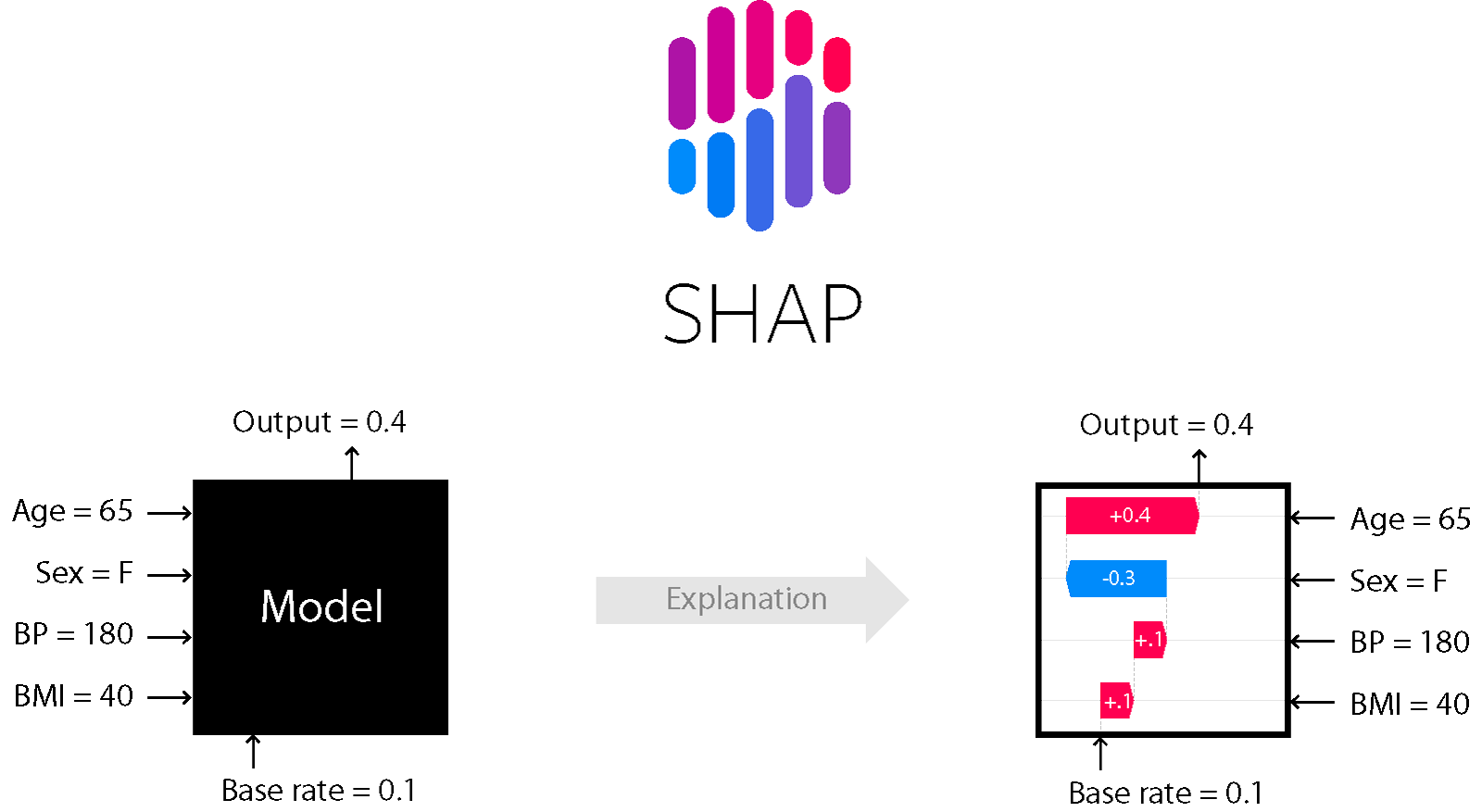

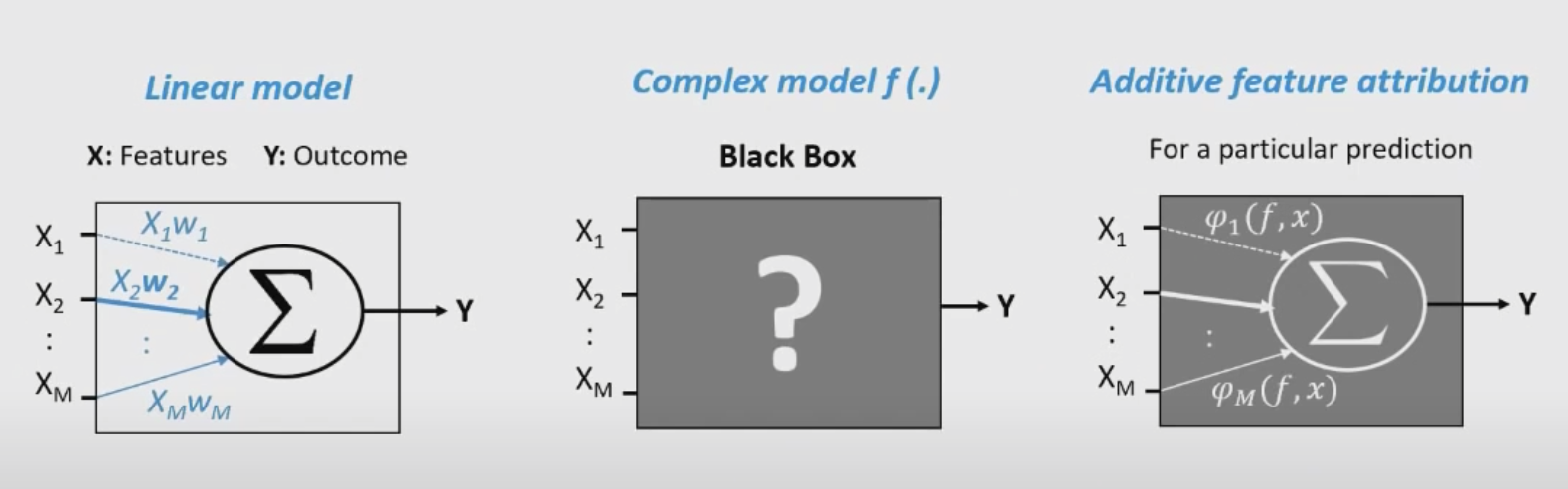

SHAP

샵라이브러리: 개별 예측 설명

- 어던 머신러닝 모델이든지 단일 관측치로부터 특성들의 기여도(feature attribution)를 계산하기 위한 방법을 배울수 있음

- sharpley value는 원래 게임이론에서 나온 개념이지만 복잡한 머신러닝모델의 예측을 설명하기 위한 매우 유용한 방법을 제공함

위에 이미지처럼 왼쪽 블랙박스 같은 모델을(뭐가 어떻게 영향주느지 알 수 없음) 오른쪽 처럼 어떤게 영향을 주는지 시각화 한 것이다.

회귀모델 예시를 사용해 진행

import numpy as np

import pandas as pd

# 킹카운티 주택가격 데이터셋을 사용

df = pd.read_csv('https://ds-lecture-data.s3.ap-northeast-2.amazonaws.com/kc_house_data/kc_house_data.csv')

# price, longitude, latitude 양 끝단 값 1% 제거합니다.

df = df[(df['price'] >= np.percentile(df['price'], 0.5)) &

(df['price'] <= np.percentile(df['price'], 99.5)) &

(df['long'] >= np.percentile(df['long'], 0.05)) &

(df['long'] <= np.percentile(df['long'], 99.95)) &

(df['lat'] >= np.percentile(df['lat'], 0.05)) &

(df['lat'] < np.percentile(df['lat'], 99.95))]

# split train/test, 시계열이니까 2015-03-01 기준으로 나눕니다

df['date'] = pd.to_datetime(df['date'], infer_datetime_format=True)

cutoff = pd.to_datetime('2015-03-01')

train = df[df['date'] < cutoff]

test = df[df['date'] >= cutoff]

train.shape, test.shape

#((16660, 21), (4691, 21))

train.columns

'''

Index(['id', 'date', 'price', 'bedrooms', 'bathrooms','sqft_living', 'sqft_lot', 'floors', 'waterfront', 'view', 'condition', 'grade',

'sqft_above', 'sqft_basement', 'yr_built', 'yr_renovated', 'zipcode', 'lat', 'long', 'sqft_living15', 'sqft_lot15'], dtype='object')

'''

#핏쳐, 타겟으로 데이터 분리

features = ['bedrooms', 'bathrooms', 'long', 'lat']

target = 'price'

X_train = train[features]

y_train = train[target]

X_test = test[features]

y_test = test[target]from scipy.stats import randint, uniform

from sklearn.ensemble import RandomForestRegressor

from sklearn.model_selection import RandomizedSearchCV

param_distributions = {

'n_estimators': randint(50, 500),

'max_depth': [5, 10, 15, 20, None],

'max_features': uniform(0, 1),

}

search = RandomizedSearchCV(

RandomForestRegressor(random_state=2),

param_distributions=param_distributions,

n_iter=5,

cv=3,

scoring='neg_mean_absolute_error',

verbose=10,

return_train_score=True,

n_jobs=-1,

random_state=2

)

search.fit(X_train, y_train);

print('최적 하이퍼파라미터: ', search.best_params_)

print('CV MAE: ', -search.best_score_)

model = search.best_estimator_

회귀 모델 핏까지 완료했고 최적 파라미터 확인 했음

sharpley values

- 게임이론에 기초한건데 같은 팀 선수들(특성들)이 게임 목표(예측) 달성을 위해 각자 자신의 역할(기여)을 한다고 할때 게임 목표 달성 후 받은 포상을 어떻게 하면 그들의 기여도에 따라 공평하게 나누어 줄 수 있을것인가?라는 질문과 연관됨

- 위에 이미지를 보면 sharply value를 머신러닝의 특성 기여도 산정에 활용하는 것을 알 수 있음

- 특성의 갯수가 많아질 수록 필요한 계산량이 기하 급수적으로 늘어나기 때문에 sharp에서는 샘플링을 이용해 근사적으로 값을 구함

pip install shap

import shap

explainer = shap.TreeExplainer(model)

shap_values = explainer.shap_values(row)

shap.initjs()

shap.force_plot(

base_value=explainer.expected_value,

shap_values=shap_values,

features=row

```

모델이 집값을 341,878.50으로 예측했는데 이는 lat=47.37, bedrooms=3 때문에 낮아지다가 bathrooms = 2.5 때문에 높아진 값으로 표를 확인하면 됨pdp와 sharp의 차이점

pdp와 특성 중요도와 차이를 가짐

shap은 데이터 샘플 하나에 대한 설명을 하는 것임

관측치 하나하나마다 특성의 영향도가 다르게 계산이 될 수 있음