평가지표로는 RMSLE를 사용하자.

데이터 전처리

데이터 탐색 후 전처리를 진행하자

여러가지 전처리를 해보기 위해 원본 데이터는 따로 저장하고, 복사본을 사용하기

import warnings

warnings.filterwarnings('ignore')

import pandas as pd

import numpy as np

import seaborn as sns

import matplotlib.pyplot as plt

house_df_org = pd.read_csv('house_price.csv') # 원본을 저장해둠

house_df = house_df_org.copy() # 이걸로 처리

house_df.head(3)

house_df.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 1460 entries, 0 to 1459

Data columns (total 81 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Id 1460 non-null int64

1 MSSubClass 1460 non-null int64

2 MSZoning 1460 non-null object

3 LotFrontage 1201 non-null float64

4 LotArea 1460 non-null int64

5 Street 1460 non-null object

6 Alley 91 non-null object

7 LotShape 1460 non-null object

8 LandContour 1460 non-null object

9 Utilities 1460 non-null object

10 LotConfig 1460 non-null object

11 LandSlope 1460 non-null object

12 Neighborhood 1460 non-null object

13 Condition1 1460 non-null object

14 Condition2 1460 non-null object

15 BldgType 1460 non-null object

16 HouseStyle 1460 non-null object

17 OverallQual 1460 non-null int64

18 OverallCond 1460 non-null int64

19 YearBuilt 1460 non-null int64

20 YearRemodAdd 1460 non-null int64

21 RoofStyle 1460 non-null object

22 RoofMatl 1460 non-null object

23 Exterior1st 1460 non-null object

24 Exterior2nd 1460 non-null object

25 MasVnrType 1452 non-null object

26 MasVnrArea 1452 non-null float64

27 ExterQual 1460 non-null object

28 ExterCond 1460 non-null object

29 Foundation 1460 non-null object

30 BsmtQual 1423 non-null object

31 BsmtCond 1423 non-null object

32 BsmtExposure 1422 non-null object

33 BsmtFinType1 1423 non-null object

34 BsmtFinSF1 1460 non-null int64

35 BsmtFinType2 1422 non-null object

36 BsmtFinSF2 1460 non-null int64

37 BsmtUnfSF 1460 non-null int64

38 TotalBsmtSF 1460 non-null int64

39 Heating 1460 non-null object

40 HeatingQC 1460 non-null object

41 CentralAir 1460 non-null object

42 Electrical 1459 non-null object

43 1stFlrSF 1460 non-null int64

44 2ndFlrSF 1460 non-null int64

45 LowQualFinSF 1460 non-null int64

46 GrLivArea 1460 non-null int64

47 BsmtFullBath 1460 non-null int64

48 BsmtHalfBath 1460 non-null int64

49 FullBath 1460 non-null int64

50 HalfBath 1460 non-null int64

51 BedroomAbvGr 1460 non-null int64

52 KitchenAbvGr 1460 non-null int64

53 KitchenQual 1460 non-null object

54 TotRmsAbvGrd 1460 non-null int64

55 Functional 1460 non-null object

56 Fireplaces 1460 non-null int64

57 FireplaceQu 770 non-null object

58 GarageType 1379 non-null object

59 GarageYrBlt 1379 non-null float64

60 GarageFinish 1379 non-null object

61 GarageCars 1460 non-null int64

62 GarageArea 1460 non-null int64

63 GarageQual 1379 non-null object

64 GarageCond 1379 non-null object

65 PavedDrive 1460 non-null object

66 WoodDeckSF 1460 non-null int64

67 OpenPorchSF 1460 non-null int64

68 EnclosedPorch 1460 non-null int64

69 3SsnPorch 1460 non-null int64

70 ScreenPorch 1460 non-null int64

71 PoolArea 1460 non-null int64

72 PoolQC 7 non-null object

73 Fence 281 non-null object

74 MiscFeature 54 non-null object

75 MiscVal 1460 non-null int64

76 MoSold 1460 non-null int64

77 YrSold 1460 non-null int64

78 SaleType 1460 non-null object

79 SaleCondition 1460 non-null object

80 SalePrice 1460 non-null int64

dtypes: float64(3), int64(35), object(43)

memory usage: 924.0+ KB칼럼이 꽤 많고, null값이 존재하는 칼럼들 꽤 있다.

좀 더 구체적으로 알아보자

print('데이터 세트의 Shape:', house_df.shape)

print('\n전체 feature 들의 type \n',house_df.dtypes.value_counts())

isnull_series = house_df.isnull().sum()

print('\nNull 컬럼과 그 건수:\n ', isnull_series[isnull_series > 0].sort_values(ascending=False)) # Null이 1개 이상 있는 칼럼만 보기데이터 세트의 Shape: (1460, 81)

전체 feature 들의 type

object 43

int64 35

float64 3

dtype: int64

Null 컬럼과 그 건수:

PoolQC 1453

MiscFeature 1406

Alley 1369

Fence 1179

FireplaceQu 690

LotFrontage 259

GarageYrBlt 81

GarageType 81

GarageFinish 81

GarageQual 81

GarageCond 81

BsmtFinType2 38

BsmtExposure 38

BsmtFinType1 37

BsmtCond 37

BsmtQual 37

MasVnrArea 8

MasVnrType 8

Electrical 1

dtype: int64object type도 꽤 많다. 이건 나중에 원핫인코딩 처리 해야할 듯

Null값이 대부분인 칼럼도 확인 됨

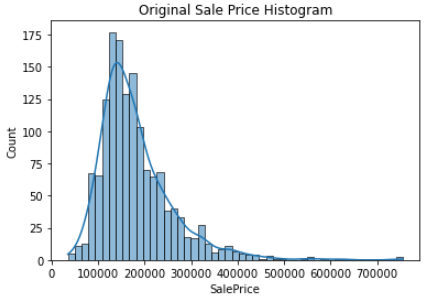

종속변수(Target)인 SalePrice의 분포도를 확인해보자

plt.title('Original Sale Price Histogram')

plt.xticks()

sns.histplot(house_df['SalePrice'], kde=True)

plt.show()

살짝 Right-skew 하다

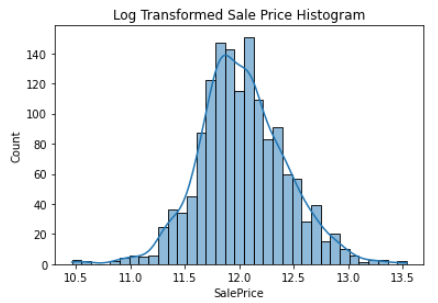

log 변환하고 분포도를 확인해보자

plt.title('Log Transformed Sale Price Histogram')

log_SalePrice = np.log1p(house_df['SalePrice'])

sns.histplot(log_SalePrice, kde=True)

plt.show()

log 변환하니까 꽤 정규분포에 가까워졌다. 이걸 사용하도록 하자

우리는 평가지표로 RMSLE를 사용한다고 했다.

여기서 log 변환된 Target 값에 대해 RMSE를 구하면 그게 RMSLE가 됨!

Null을 가지는 칼럼을 Series로 뽑아내고,

dtypes를 출력해보자

null_column_count = house_df.isnull().sum()[house_df.isnull().sum() > 0]

house_df.dtypes[null_column_count.index]LotFrontage float64

Alley object

MasVnrType object

MasVnrArea float64

BsmtQual object

BsmtCond object

BsmtExposure object

BsmtFinType1 object

BsmtFinType2 object

Electrical object

FireplaceQu object

GarageType object

GarageYrBlt float64

GarageFinish object

GarageQual object

GarageCond object

PoolQC object

Fence object

MiscFeature object

dtype: object

- SalePrice에 대해 log 변환 진행 (위에서는 그림만 그렸음)

- Null이 너무 많은 칼럼은 삭제

- 남은 수치형 칼럼은 평균값 대체

- 남은 object 칼럼 리스트를 출력

# SalePrice 로그 변환

# 두 번 돌리면 안 됨! 로그변환 한 것을 또 로그변환 해버림

original_SalePrice = house_df['SalePrice']

house_df['SalePrice'] = np.log1p(house_df['SalePrice'])

# Null 이 너무 많은 컬럼들과 불필요한 컬럼 삭제

house_df.drop(['Id','PoolQC' , 'MiscFeature', 'Alley', 'Fence','FireplaceQu'], axis=1 , inplace=True)

# Drop 하지 않는 숫자형 Null컬럼들은 평균값으로 대체

house_df.fillna(house_df.mean(),inplace=True)

# Null 값이 있는 피처명과 타입을 추출

null_column_count = house_df.isnull().sum()[house_df.isnull().sum() > 0]

print('## Null 피처의 Type :\n', house_df.dtypes[null_column_count.index])## Null 피처의 Type :

MasVnrType object

BsmtQual object

BsmtCond object

BsmtExposure object

BsmtFinType1 object

BsmtFinType2 object

Electrical object

GarageType object

GarageFinish object

GarageQual object

GarageCond object

dtype: object원핫인코딩 수행한 데이터프레임을 house_df_ohe에 저장

print('get_dummies() 수행 전 데이터 Shape:', house_df.shape)

house_df_ohe = pd.get_dummies(house_df)

print('get_dummies() 수행 후 데이터 Shape:', house_df_ohe.shape)

null_column_count = house_df_ohe.isnull().sum()[house_df_ohe.isnull().sum() > 0]

print('## Null 피처의 Type :\n', house_df_ohe.dtypes[null_column_count.index])get_dummies() 수행 전 데이터 Shape: (1460, 75)

get_dummies() 수행 후 데이터 Shape: (1460, 271)

## Null 피처의 Type :

Series([], dtype: object)선형 회귀 모델 학습/예측/평가

위에서 말한 것처럼 log 변환된 Target 값에 대해 RMSE를 구하면 그게 RMSLE가 됨!

여러 모델을 돌려볼 것이기 때문에 예측/평가는 함수로 만들어두고, 후에 학습만 개별적으로 진행하자

# 학습이 완료된 모델을 인자로 받아서 테스트 데이터로 예측하고 RMSE를 계산

def get_rmse(model):

pred = model.predict(X_test)

# y_test, pred는 로그 스케일임.

mse = mean_squared_error(y_test , pred)

rmse = np.sqrt(mse)

print('{0} 로그 변환된 RMSE: {1}'.format(model.__class__.__name__,np.round(rmse, 3)))

return rmse

# 여러 모델들을 list 형태로 인자로 받아서 개별 모델들의 RMSE를 list로 반환.

def get_rmses(models):

rmses = [ ]

for model in models:

rmse = get_rmse(model)

rmses.append(rmse)

return rmsesLinear/Ridge/Lasso Regression 각각 학습 예측 평가 수행

from sklearn.linear_model import LinearRegression, Ridge, Lasso

from sklearn.model_selection import train_test_split

from sklearn.metrics import mean_squared_error

y_target = house_df_ohe['SalePrice']

X_features = house_df_ohe.drop('SalePrice',axis=1, inplace=False)

X_train, X_test, y_train, y_test = train_test_split(X_features, y_target, test_size=0.2, random_state=156)

# LinearRegression, Ridge, Lasso 학습, 예측, 평가

lr_reg = LinearRegression()

lr_reg.fit(X_train, y_train)

ridge_reg = Ridge()

ridge_reg.fit(X_train, y_train)

lasso_reg = Lasso()

lasso_reg.fit(X_train, y_train)

models = [lr_reg, ridge_reg, lasso_reg]

get_rmses(models)LinearRegression 로그 변환된 RMSE: 0.132

Ridge 로그 변환된 RMSE: 0.128

Lasso 로그 변환된 RMSE: 0.176

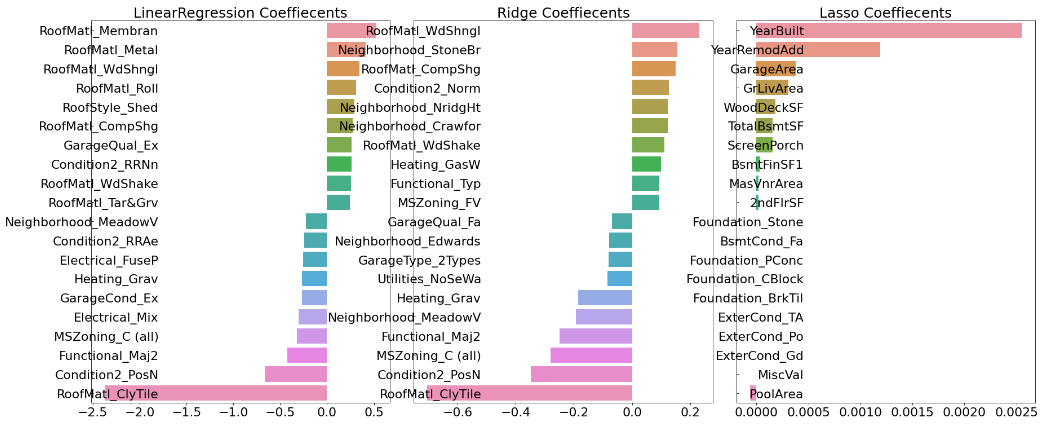

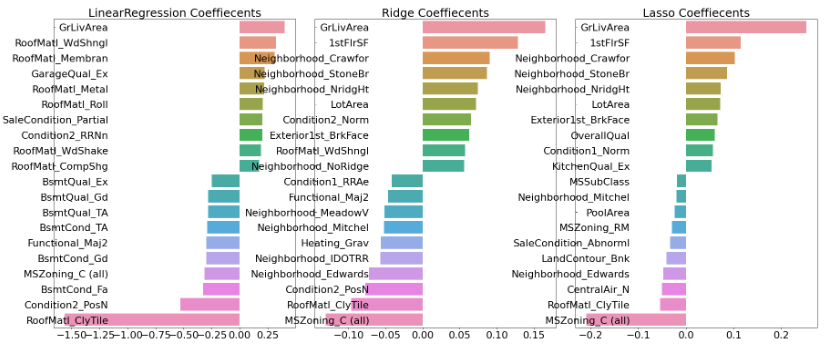

[0.1318957657915436, 0.12750846334053045, 0.17628250556471395]Lasso가 좀 별로이고, Ridge가 제일 잘 나왔다.

각 회귀 계수를 시각화해보자 상위 10개, 하위 10개의 회귀 계수 값을 Series로 생성하는 함수 만들기

def get_top_bottom_coef(model):

# coef_ 속성을 기반으로 Series 객체를 생성. index는 컬럼명.

coef = pd.Series(model.coef_, index=X_features.columns)

# + 상위 10개 , - 하위 10개 coefficient 추출하여 반환.

coef_high = coef.sort_values(ascending=False).head(10)

coef_low = coef.sort_values(ascending=False).tail(10)

return coef_high, coef_low세 가지 모델에 대해서 시각화 진행

def visualize_coefficient(models):

# 3개 회귀 모델의 시각화를 위해 3개의 컬럼을 가지는 subplot 생성

fig, axs = plt.subplots(figsize=(24,10),nrows=1, ncols=3)

fig.tight_layout()

# 입력인자로 받은 list객체인 models에서 차례로 model을 추출하여 회귀 계수 시각화.

for i_num, model in enumerate(models):

# 상위 10개, 하위 10개 회귀 계수를 구하고, 이를 판다스 concat으로 결합.

coef_high, coef_low = get_top_bottom_coef(model)

coef_concat = pd.concat( [coef_high , coef_low] )

# 순차적으로 ax subplot에 barchar로 표현. 한 화면에 표현하기 위해 tick label 위치와 font 크기 조정.

axs[i_num].set_title(model.__class__.__name__+' Coeffiecents', size=25)

axs[i_num].tick_params(axis="y",direction="in", pad=-120)

for label in (axs[i_num].get_xticklabels() + axs[i_num].get_yticklabels()):

label.set_fontsize(22)

sns.barplot(x=coef_concat.values, y=coef_concat.index , ax=axs[i_num])

# 앞 예제에서 학습한 lr_reg, ridge_reg, lasso_reg 모델의 회귀 계수 시각화.

models = [lr_reg, ridge_reg, lasso_reg]

visualize_coefficient(models)

전체에 대해서 교차 검증을 진행

타겟값을 로그 변환 했으니까 실제로는 RMSLE를 구한 것임

from sklearn.model_selection import cross_val_score

def get_avg_rmse_cv(models):

for model in models:

# 분할하지 않고 전체 데이터로 cross_val_score( ) 수행. 모델별 CV RMSE값과 평균 RMSE 출력

rmse_list = np.sqrt(-cross_val_score(model, X_features, y_target,

scoring="neg_mean_squared_error", cv = 5))

rmse_avg = np.mean(rmse_list)

print('\n{0} CV RMSE 값 리스트: {1}'.format( model.__class__.__name__, np.round(rmse_list, 3)))

print('{0} CV 평균 RMSE 값: {1}'.format( model.__class__.__name__, np.round(rmse_avg, 3)))

# 앞 예제에서 학습한 ridge_reg, lasso_reg 모델의 CV RMSE값 출력

models = [ridge_reg, lasso_reg]

get_avg_rmse_cv(models)Ridge CV RMSE 값 리스트: [0.117 0.154 0.142 0.117 0.189]

Ridge CV 평균 RMSE 값: 0.144

Lasso CV RMSE 값 리스트: [0.161 0.204 0.177 0.181 0.265]

Lasso CV 평균 RMSE 값: 0.198Ridge가 좀 더 우수한 성능을 보인다.

alpha값을 변겨해 하면서 그리드서치 진행

from sklearn.model_selection import GridSearchCV

def print_best_params(model, params):

grid_model = GridSearchCV(model, param_grid=params,

scoring='neg_mean_squared_error', cv=5)

grid_model.fit(X_features, y_target)

rmse = np.sqrt(-1* grid_model.best_score_)

print('{0} 5 CV 시 최적 평균 RMSE 값: {1}, 최적 alpha:{2}'.format(model.__class__.__name__,

np.round(rmse, 4), grid_model.best_params_))

return grid_model.best_estimator_

ridge_params = { 'alpha':[0.05, 0.1, 1, 5, 8, 10, 12, 15, 20] }

lasso_params = { 'alpha':[0.001, 0.005, 0.008, 0.05, 0.03, 0.1, 0.5, 1,5, 10] }

best_rige = print_best_params(ridge_reg, ridge_params)

best_lasso = print_best_params(lasso_reg, lasso_params)Ridge 5 CV 시 최적 평균 RMSE 값: 0.1418, 최적 alpha:{'alpha': 12}

Lasso 5 CV 시 최적 평균 RMSE 값: 0.142, 최적 alpha:{'alpha': 0.001}그리드 서치 진행해보니 둘이 거의 유사하다.

각각 최적화된 alpha 값으로 학습 데이터과 테스트 데이터로 예측 및 평가를 수행하고, 회귀 계수 시각화까지 진행

# 앞의 최적화 alpha값으로 학습데이터로 학습, 테스트 데이터로 예측 및 평가 수행.

lr_reg = LinearRegression()

lr_reg.fit(X_train, y_train)

ridge_reg = Ridge(alpha=12)

ridge_reg.fit(X_train, y_train)

lasso_reg = Lasso(alpha=0.001)

lasso_reg.fit(X_train, y_train)

# 모든 모델의 RMSE 출력

models = [lr_reg, ridge_reg, lasso_reg]

get_rmses(models)

# 모든 모델의 회귀 계수 시각화

models = [lr_reg, ridge_reg, lasso_reg]

visualize_coefficient(models)LinearRegression 로그 변환된 RMSE: 0.132

Ridge 로그 변환된 RMSE: 0.124

Lasso 로그 변환된 RMSE: 0.12

object가 아닌 칼럼 (수치형 칼럼)에 대해 skew 정도를 확인해보자

skew가 1이 넘는 칼럼들만 출력

from scipy.stats import skew

# object가 아닌 숫자형 피쳐의 컬럼 index 객체 추출.

features_index = house_df.dtypes[house_df.dtypes != 'object'].index

# house_df에 컬럼 index를 [ ]로 입력하면 해당하는 컬럼 데이터 셋 반환. apply lambda로 skew( )호출

skew_features = house_df[features_index].apply(lambda x : skew(x))

# skew 정도가 1 이상인 컬럼들만 추출.

skew_features_top = skew_features[skew_features > 1]

print(skew_features_top.sort_values(ascending=False))MiscVal 24.451640

PoolArea 14.813135

LotArea 12.195142

3SsnPorch 10.293752

LowQualFinSF 9.002080

KitchenAbvGr 4.483784

BsmtFinSF2 4.250888

ScreenPorch 4.117977

BsmtHalfBath 4.099186

EnclosedPorch 3.086696

MasVnrArea 2.673661

LotFrontage 2.382499

OpenPorchSF 2.361912

BsmtFinSF1 1.683771

WoodDeckSF 1.539792

TotalBsmtSF 1.522688

MSSubClass 1.406210

1stFlrSF 1.375342

GrLivArea 1.365156

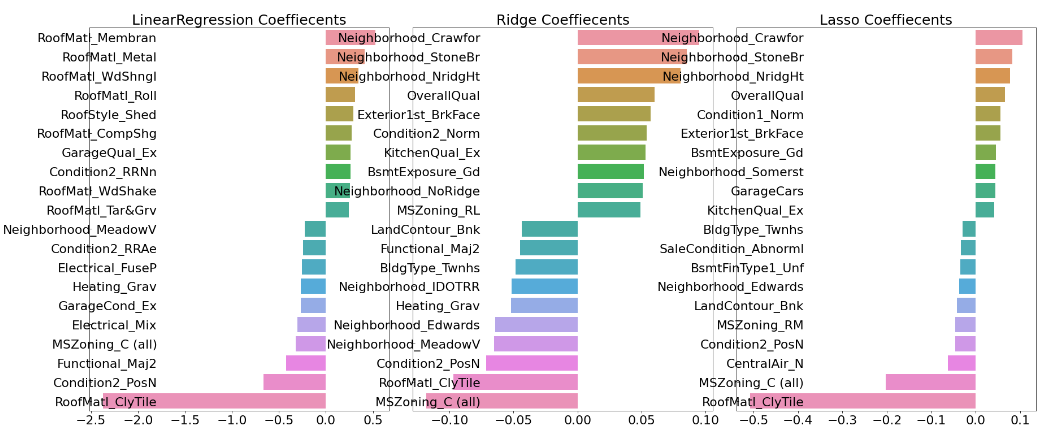

dtype: float64skew가 1보다 큰 칼럼들에 대해 log 변환을 적용하고, 다시 하이퍼 파라미터 튜닝 후 학습/예측/평가 해보자

house_df[skew_features_top.index] = np.log1p(house_df[skew_features_top.index])# Skew가 높은 피처들을 로그 변환 했으므로 다시 원-핫 인코딩 적용 및 피처/타겟 데이터 셋 생성,

house_df_ohe = pd.get_dummies(house_df)

y_target = house_df_ohe['SalePrice']

X_features = house_df_ohe.drop('SalePrice',axis=1, inplace=False)

X_train, X_test, y_train, y_test = train_test_split(X_features, y_target, test_size=0.2, random_state=156)

# 피처들을 로그 변환 후 다시 최적 하이퍼 파라미터와 RMSE 출력

ridge_params = { 'alpha':[0.05, 0.1, 1, 5, 8, 10, 12, 15, 20] }

lasso_params = { 'alpha':[0.001, 0.005, 0.008, 0.05, 0.03, 0.1, 0.5, 1,5, 10] }

best_ridge = print_best_params(ridge_reg, ridge_params)

best_lasso = print_best_params(lasso_reg, lasso_params)Ridge 5 CV 시 최적 평균 RMSE 값: 0.1275, 최적 alpha:{'alpha': 10}

Lasso 5 CV 시 최적 평균 RMSE 값: 0.1252, 최적 alpha:{'alpha': 0.001# 앞의 최적화 alpha값으로 학습데이터로 학습, 테스트 데이터로 예측 및 평가 수행.

lr_reg = LinearRegression()

lr_reg.fit(X_train, y_train)

ridge_reg = Ridge(alpha=10)

ridge_reg.fit(X_train, y_train)

lasso_reg = Lasso(alpha=0.001)

lasso_reg.fit(X_train, y_train)

# 모든 모델의 RMSE 출력

models = [lr_reg, ridge_reg, lasso_reg]

get_rmses(models)

# 모든 모델의 회귀 계수 시각화

models = [lr_reg, ridge_reg, lasso_reg]

visualize_coefficient(models)LinearRegression 로그 변환된 RMSE: 0.128

Ridge 로그 변환된 RMSE: 0.122

Lasso 로그 변환된 RMSE: 0.119

성능 향상이 조금 있었다.

이제 이상치 처리를 진행하자

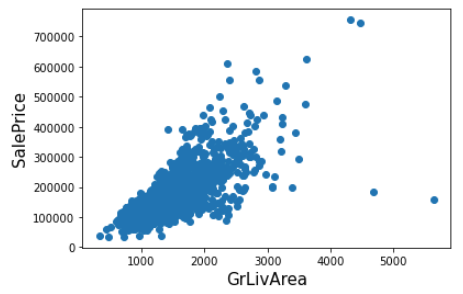

회귀 계수가 높아서 주요 Feature로 확인 되는 GrLivArea에 대해 산점도를 나타내자

plt.scatter(x = house_df_org['GrLivArea'], y = house_df_org['SalePrice'])

plt.ylabel('SalePrice', fontsize=15)

plt.xlabel('GrLivArea', fontsize=15)

plt.show()

GrLivArea와 SalePrice에 대해서 log 변환을 고려한 조건을 지정해서, 이상치를 제거하자

# GrLivArea와 SalePrice 모두 로그 변환되었으므로 이를 반영한 조건 생성.

cond1 = house_df_ohe['GrLivArea'] > np.log1p(4000)

cond2 = house_df_ohe['SalePrice'] < np.log1p(500000)

outlier_index = house_df_ohe[cond1 & cond2].index

print('아웃라이어 레코드 index :', outlier_index.values)

print('아웃라이어 삭제 전 house_df_ohe shape:', house_df_ohe.shape)

# DataFrame의 index를 이용하여 아웃라이어 레코드 삭제.

house_df_ohe.drop(outlier_index , axis=0, inplace=True)

print('아웃라이어 삭제 후 house_df_ohe shape:', house_df_ohe.shape)아웃라이어 레코드 index : [ 523 1298]

아웃라이어 삭제 전 house_df_ohe shape: (1460, 271)

아웃라이어 삭제 후 house_df_ohe shape: (1458, 271)2개의 행이 제거된 것으로 확인 된다.

이상치를 제거할 때는 행을 제거하니까axis=0인 것을 잊지 말기

이상치 제거 후 다시 그리드 서치를 진행하자!

y_target = house_df_ohe['SalePrice']

X_features = house_df_ohe.drop('SalePrice',axis=1, inplace=False)

X_train, X_test, y_train, y_test = train_test_split(X_features, y_target, test_size=0.2, random_state=156)

ridge_params = { 'alpha':[0.05, 0.1, 1, 5, 8, 10, 12, 15, 20] }

lasso_params = { 'alpha':[0.001, 0.005, 0.008, 0.05, 0.03, 0.1, 0.5, 1,5, 10] }

best_ridge = print_best_params(ridge_reg, ridge_params)

best_lasso = print_best_params(lasso_reg, lasso_params)Ridge 5 CV 시 최적 평균 RMSE 값: 0.1125, 최적 alpha:{'alpha': 8}

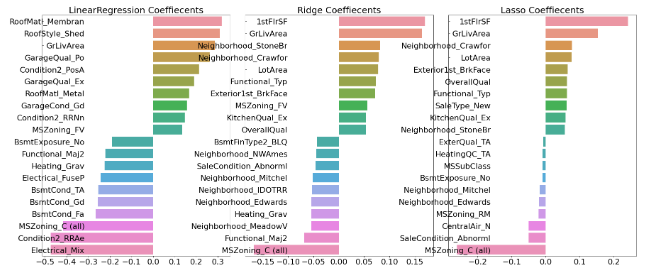

Lasso 5 CV 시 최적 평균 RMSE 값: 0.1122, 최적 alpha:{'alpha': 0.001}# 앞의 최적화 alpha값으로 학습데이터로 학습, 테스트 데이터로 예측 및 평가 수행.

lr_reg = LinearRegression()

lr_reg.fit(X_train, y_train)

ridge_reg = Ridge(alpha=8)

ridge_reg.fit(X_train, y_train)

lasso_reg = Lasso(alpha=0.001)

lasso_reg.fit(X_train, y_train)

# 모든 모델의 RMSE 출력

models = [lr_reg, ridge_reg, lasso_reg]

get_rmses(models)

# 모든 모델의 회귀 계수 시각화

models = [lr_reg, ridge_reg, lasso_reg]

visualize_coefficient(models)LinearRegression 로그 변환된 RMSE: 0.129

Ridge 로그 변환된 RMSE: 0.103

Lasso 로그 변환된 RMSE: 0.1

역시 이상치만 잘 제거해도 성능이 꽤 향상 된다.

하지만 이상치 처리는 테스트 데이터에도 이런 데이터가 있을지를 잘 고려해야한다.

최대한 보수적으로 진행!

처리 후 GrLivArea의 회귀 계수가 조금 조정된 듯 보인다.

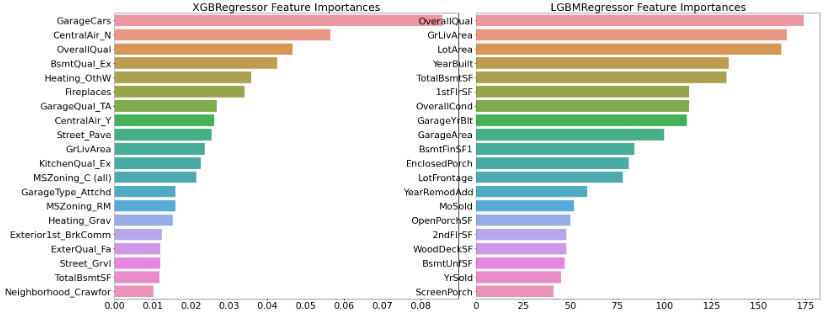

회귀 트리 계열 학습/예측/평가

이번엔 트리 계열 모델인 XGBoost와 LightGBM을 사용하자

학습 시간 관계상 각각n_estimators=1000으로만 설정하고 교차 검증을 진행

->print_best_parmas()를 사용하지만 실제로는 파라미터 하나 뿐

from xgboost import XGBRegressor

xgb_params = {'n_estimators':[1000]}

xgb_reg = XGBRegressor(n_estimators=1000, learning_rate=0.05,

colsample_bytree=0.5, subsample=0.8)

best_xgb = print_best_params(xgb_reg, xgb_params)XGBRegressor 5 CV 시 최적 평균 RMSE 값: 0.1178, 최적 alpha:{'n_estimators': 1000}from lightgbm import LGBMRegressor

lgbm_params = {'n_estimators':[1000]}

lgbm_reg = LGBMRegressor(n_estimators=1000, learning_rate=0.05, num_leaves=4,

subsample=0.6, colsample_bytree=0.4, reg_lambda=10, n_jobs=-1)

best_lgbm = print_best_params(lgbm_reg, lgbm_params)LGBMRegressor 5 CV 시 최적 평균 RMSE 값: 0.1163, 최적 alpha:{'n_estimators': 1000}각각 Feature Importance를 시각화하자

# 모델의 중요도 상위 20개의 피처명과 그때의 중요도값을 Series로 반환.

def get_top_features(model):

ftr_importances_values = model.feature_importances_

ftr_importances = pd.Series(ftr_importances_values, index=X_features.columns )

ftr_top20 = ftr_importances.sort_values(ascending=False)[:20]

return ftr_top20

def visualize_ftr_importances(models):

# 2개 회귀 모델의 시각화를 위해 2개의 컬럼을 가지는 subplot 생성

fig, axs = plt.subplots(figsize=(24,10),nrows=1, ncols=2)

fig.tight_layout()

# 입력인자로 받은 list객체인 models에서 차례로 model을 추출하여 피처 중요도 시각화.

for i_num, model in enumerate(models):

# 중요도 상위 20개의 피처명과 그때의 중요도값 추출

ftr_top20 = get_top_features(model)

axs[i_num].set_title(model.__class__.__name__+' Feature Importances', size=25)

#font 크기 조정.

for label in (axs[i_num].get_xticklabels() + axs[i_num].get_yticklabels()):

label.set_fontsize(22)

sns.barplot(x=ftr_top20.values, y=ftr_top20.index , ax=axs[i_num])

# 앞 예제에서 print_best_params( )가 반환한 GridSearchCV로 최적화된 모델의 피처 중요도 시각화

models = [best_xgb, best_lgbm]

visualize_ftr_importances(models)

혼합 예측

앙상블과 비슷한 것으로 생각하면 됨

estimator.predict(test)한 것을 가중 평균을 내면 됨!

여기서는0.4 * ridge_pred + 0.6 * lasso_pred로 고정했는데,

실제로는 가중치를 바꿔가면서 성능이 좋은 것을 선택!

def get_rmse_pred(preds):

for key in preds.keys():

pred_value = preds[key]

mse = mean_squared_error(y_test , pred_value)

rmse = np.sqrt(mse)

print('{0} 모델의 RMSE: {1}'.format(key, rmse))

# 개별 모델의 학습

ridge_reg = Ridge(alpha=8)

ridge_reg.fit(X_train, y_train)

lasso_reg = Lasso(alpha=0.001)

lasso_reg.fit(X_train, y_train)

# 개별 모델 예측

ridge_pred = ridge_reg.predict(X_test)

lasso_pred = lasso_reg.predict(X_test)

# 개별 모델 예측값 혼합으로 최종 예측값 도출

pred = 0.4 * ridge_pred + 0.6 * lasso_pred

preds = {'최종 혼합': pred,

'Ridge': ridge_pred,

'Lasso': lasso_pred}

#최종 혼합 모델, 개별모델의 RMSE 값 출력

get_rmse_pred(preds)최종 혼합 모델의 RMSE: 0.10007930884470519

Ridge 모델의 RMSE: 0.10345177546603272

Lasso 모델의 RMSE: 0.10024170460890039xgb_reg = XGBRegressor(n_estimators=1000, learning_rate=0.05,

colsample_bytree=0.5, subsample=0.8)

lgbm_reg = LGBMRegressor(n_estimators=1000, learning_rate=0.05, num_leaves=4,

subsample=0.6, colsample_bytree=0.4, reg_lambda=10, n_jobs=-1)

xgb_reg.fit(X_train, y_train)

lgbm_reg.fit(X_train, y_train)

xgb_pred = xgb_reg.predict(X_test)

lgbm_pred = lgbm_reg.predict(X_test)

pred = 0.5 * xgb_pred + 0.5 * lgbm_pred

preds = {'최종 혼합': pred,

'XGBM': xgb_pred,

'LGBM': lgbm_pred}

get_rmse_pred(preds)최종 혼합 모델의 RMSE: 0.10170077353447762

XGBM 모델의 RMSE: 0.10738295638346222

LGBM 모델의 RMSE: 0.10382510019327311스태킹 모델을 이용한 예측

스태킹 먼저 작성 후 나머지 작성